| |

THIS WEEK'S KEYS:Pulse: The Digital Shift in HVAC Distribution Playbook: Preferred Equity: The New Deal Lever Spotlight: The Rise of Private Credit in the Lower Middle Market Roundup: This Week’s M&A Highlights

Have a great weekend! | | |

| | | PULSE The Digital Shift in HVAC Distribution |  | | |

|

|

|---|

The opportunity in HVAC distribution remains large and increasingly digital. According to industry data from the Air-Conditioning, Heating, and Refrigeration Institute, the North American HVAC equipment and distribution market exceeds ~$60 billion annually and continues to grow at a mid-single-digit pace. The demand backdrop is structurally strong. Energy efficiency mandates, electrification trends, smart home adoption, and the accelerating transition to heat pump systems are all expanding end-market demand. At the same time, the way that demand is accessed is shifting, with digital platforms becoming a central component of how contractors and procurement teams source products.

Scale remains concentrated at the top of the market, but competitive dynamics are evolving. According to ACHR News, the four largest HVACR distributors generated a combined ~$13.8 billion in revenue in 2024, with each investing heavily in digital ordering systems, mobile-first tools, and integrated customer platforms. Historically, distribution advantage was defined by branch density, inventory availability, and local relationships. Those factors still matter, but they are increasingly being complemented by digital capabilities that influence purchasing behavior, pricing transparency, and customer retention.

Customer expectations have already moved ahead of many distributors. McKinsey & Company notes that B2B buyers now use up to ten different purchasing channels, up from five in 2016. This reflects a broader shift in how contractors and procurement teams operate. Purchasing is no longer confined to counter sales or account managers. Buyers increasingly expect real-time pricing, accurate inventory visibility, seamless mobile ordering, and integrated fulfillment. Distributors that have adapted to this omnichannel reality are seeing measurable performance gains, with McKinsey estimating revenue growth of ~5% to 15% for omnichannel adopters. Those that lag risk being disintermediated or pushed into lower-margin fulfillment roles.

Ferguson plc provides one of the clearest case studies of this transition. The company has paired its physical footprint with significant digital investment, expanding its product assortment from ~1 million to ~3.5 million SKUs while building out its e-commerce infrastructure. According to Digital Commerce 360, Ferguson generated ~$515.8 million in digital sales in a single quarter, representing ~7% of U.S. revenue. At the same time, its residential e-commerce declined ~8% year over year amid softer demand, highlighting an important reality. Digital channels do not eliminate volatility. They change where it shows up. With more than 1,500 branches, Ferguson is building a hybrid model where physical distribution and digital execution reinforce each other rather than compete.

The implications extend beyond revenue growth. Digital platforms are increasingly becoming operational infrastructure rather than simply sales channels. Real-time pricing engines improve margin discipline. Automated procurement reduces administrative burden. Integrated inventory systems enhance working capital efficiency and reduce stockouts. As supply chains remain complex and input costs fluctuate, these capabilities are becoming central to maintaining performance.

At the same time, the industry continues to face meaningful headwinds. Tariff uncertainty, labor shortages and the transition to next-generation refrigerants are all adding pressure to cost structures. The phased shift toward lower global warming potential refrigerants is expected to increase equipment and installation costs across the HVAC ecosystem. Labor constraints remain persistent, with contractors struggling to recruit and retain skilled technicians even as demand remains stable. These factors increase execution complexity and place greater importance on operational efficiency.

Importantly, these pressures are reinforcing the case for digital adoption rather than slowing it. As complexity increases, the value of better systems becomes more pronounced. Distributors and contractors that leverage digital tools to improve visibility, pricing, and execution are better positioned to navigate volatility. Those who rely solely on traditional models are increasingly at risk of falling behind.

The direction of the market is becoming clearer. HVAC distribution is evolving from a branch-centric, relationship-driven model into an integrated platform that combines physical scale with digital execution. The distributors that successfully make this transition will capture a disproportionate share. Those that do not risk becoming commoditized within a more competitive and more transparent ecosystem. |

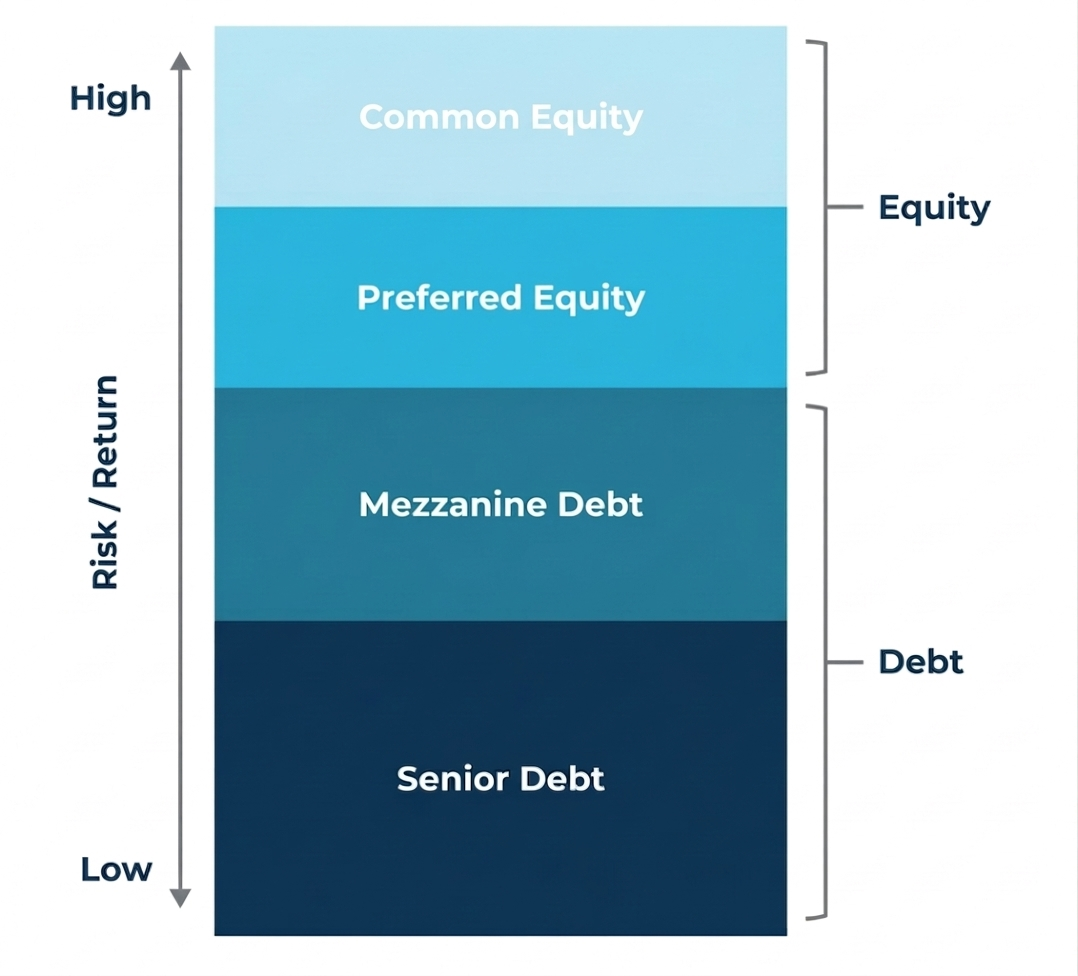

| | | PLAYBOOK Preferred Equity: The New Deal Lever |  | | | The lower middle market is operating in a more constrained capital environment. Higher interest rates have increased the cost of senior debt, while equity remains expensive and dilutive. As a result, sponsors and business owners are increasingly turning to preferred equity as a structural solution that sits between traditional debt and common equity.

Preferred equity has emerged as a flexible tool to bridge gaps in capital structures. In many transactions it functions as a release valve, allowing deals to proceed without overleveraging the business or forcing sponsors to contribute additional equity at lower returns. This dynamic has become more pronounced as credit conditions tighten. Data from Raymond James shows that interest coverage ratios in the lower middle market declined to ~2.3x in the fourth quarter of 2025 from ~2.7x earlier in the year, reflecting growing pressure on borrowers’ ability to service debt.

In this environment, preferred equity provides a practical alternative to incremental senior leverage. Unlike traditional debt, which requires consistent cash interest payments and strict covenants, preferred equity can be structured with greater flexibility. Many instruments incorporate payment-in-kind features, allowing returns to accrue rather than requiring immediate cash outflows. This preserves liquidity at the operating level and gives companies additional time to execute growth initiatives, complete integrations or stabilize performance following an acquisition.

The rise of preferred equity is also a function of capital supply. Private credit and private equity firms are sitting on significant levels of undeployed capital. According to Capstone Partners, dry powder within U.S. direct lending funds reached a record $146 billion at the end of 2025. With competition intensifying and senior loan spreads compressing to levels as low as SOFR +475bps in some segments, lenders are increasingly moving up the capital structure to capture higher returns. Preferred equity offers an attractive risk-adjusted yield profile in a market where traditional lending spreads have tightened.

From a structuring perspective, preferred equity is particularly well suited for buy-and-build strategies that dominate the lower middle market. Add-on acquisitions, integration costs and working capital needs often create funding requirements that exceed what senior lenders are willing to provide. Preferred equity fills that gap without disrupting existing debt agreements or requiring full equity dilution. It allows sponsors to maintain control while continuing to scale the platform.

However, the flexibility of preferred equity comes with tradeoffs. Because it sits below senior debt in the capital structure, it carries a higher risk profile. In downside scenarios preferred equity holders are repaid only after senior obligations are satisfied. This risk has become more relevant as credit conditions show early signs of stress. S&P Global Market Intelligence estimates that private credit default rates have risen to ~5%, up from ~3% during the 2021 to 2022 period. The increasing use of payment-in-kind structures also suggests that some borrowers are already managing elevated debt burdens by deferring cash payments.

These dynamics reinforce the importance of disciplined underwriting and thoughtful structuring. Preferred equity is most effective when paired with businesses that have clear paths to growth, strong cash flow visibility and identifiable operational improvements. In the absence of those factors, the additional layer of capital can amplify risk rather than mitigate it.

The broader takeaway is that preferred equity is no longer a niche instrument. It has become a core component of capital structures in the lower middle market. In a financing environment defined by higher borrowing costs and increased competition for deals, preferred equity allows transactions to move forward while balancing risk between debt and equity. For sponsors and operators, the use of preferred equity is less about financial engineering and more about maintaining strategic flexibility. In a market where access to capital is no longer frictionless, the ability to structure creatively has become a key differentiator. |

|

|

|

|---|

|

SPOTLIGHT The Rise of Private Credit in the Lower Middle Market |  | | | Private credit has evolved from a niche financing alternative into one of the fastest growing segments of global capital markets. Broadly defined as lending provided by non-bank institutions, private credit has become a core source of financing for companies and a critical asset class for institutional investors seeking yield and diversification.

The expansion of private credit can be traced back to the aftermath of the 2008 financial crisis. In response to the crisis regulators imposed stricter capital requirements and tighter lending standards on traditional banks. These changes reduced banks’ willingness to extend credit to middle market companies and highly leveraged borrowers. The resulting gap in capital availability created an opening for private lenders to step in and provide financing where banks pulled back. Since then the market has grown rapidly. Global private credit assets under management have expanded from ~$375 billion in the early 2010s to more than $1.6 trillion by 2023, with several industry estimates placing the market closer to $2 trillion to $3 trillion today. Much of this growth has been driven by direct lending to middle market companies, particularly those backed by private equity sponsors. In many cases private credit has become the default financing solution for sponsor-backed transactions.

The lower middle market has been a key beneficiary of this shift. Companies generating ~$5 million to $25 million in EBITDA occupy a segment that has historically been underserved by traditional capital markets. These businesses are often too large for small business lending yet too small to efficiently access syndicated loan markets or public debt. Private credit has increasingly filled this gap by providing tailored financing solutions that align with the needs of these companies.

Flexibility remains one of the defining advantages of private credit in this segment. Traditional bank loans tend to follow standardized underwriting frameworks and rigid covenant structures. Private lenders on the other hand can design bespoke capital solutions that reflect the specific characteristics of each borrower. These structures often include unitranche loans, customized covenant packages and hybrid debt solutions that simplify the capital stack. This flexibility has made private credit particularly attractive to private equity sponsors seeking certainty and efficiency in deal execution. PitchBook research highlights that direct lenders are now frequently the preferred financing partners in lower middle market buyouts.

Speed of execution further differentiates private credit from traditional bank lending. Bank loans typically require multiple layers of approval and regulatory oversight which can extend timelines significantly. Private credit funds operate with smaller investment committees and more streamlined processes allowing transactions to close in a matter of weeks rather than months. Bain & Company notes that direct lending transactions in the lower middle market can often be executed within compressed timelines, giving sponsors a competitive advantage in auction processes.

Investor demand has also been a major driver of growth. Institutional investors including pension funds, insurance companies and endowments have increased allocations to private credit in search of stable income and portfolio diversification. Many private credit instruments feature floating rate structures which have become particularly attractive in a higher interest rate environment. According to BlackRock, floating rate loans have provided investors with a degree of protection against rising rates while maintaining relatively stable income streams.

Despite its growth the asset class is not without risk. Lower middle market borrowers are often more exposed to economic cycles and company-specific challenges than larger corporations. As a result, disciplined underwriting remains critical. Leading credit managers emphasize conservative leverage structures, strong covenant protection and deep sector expertise to manage downside risk. Data from Preqin suggests that managers with specialized industry knowledge and consistent underwriting standards have historically delivered more stable performance across credit cycles.

Private credit has become a central component of the financing ecosystem for lower middle market companies. As regulatory constraints continue to shape bank lending and institutional demand for yield remains strong, private lenders are likely to play an increasingly important role in funding growth across the segment. The evolution of private credit is no longer cyclical or opportunistic. It reflects a structural shift in how capital is delivered to businesses operating outside traditional lending channels. |

|

|

|

|---|

|

| | This Week’s M&A Highlights |  |

|

|

|---|

|

●Knox Lane-backed Ruppert Landscape acquired Landscapes Unlimited, a Wilmington, NC-based lawn and landscape manager

●Home Depot (NYSE: HD)-backed Heritage Landscape Supply Group acquired Heritage Nursery, a Nebraska-based distributor of nursery products and live goods

●Red Dot Corporation acquired the assets of TSI Products and its subsidiary, International Climate Systems, both HVAC system manufacturers

●Suntex Enterprises (OTC: SNTX) acquired Deep South Electrical Contractors and GoldenEra Development, two operating subsidiaries backed by Golden Triangle Ventures

●Bain Capital acquired Duravent Group, a Detroit-based multi-brand HVAC platform

●Stonebridge Partners acquired CVM Electric, a Buffalo, NY-based commercial electrical contractor

●Audax Group acquired AKAM, a residential and commercial property manager, from Nautic Partners |

|

|

|---|

|

ABOUT US WestGate Partners | | | WestGate Partners (WGP) is an independent sponsor focused on acquiring and growing lower middle market businesses in essential residential and commercial services. We bring institutional experience, tailored capital with hands-on partnership to help owners transition, grow and preserve their legacy. By partnering with strong operators, we build enduring businesses in economically-insulated industries. |

|

|

|

|---|

|

For more information, please visit: |

|

|

| | |

|---|

|

|